There are sayings such as: “It’s always darkest before the dawn” and “There’s a silver lining to every cloud.” Translating this to Wall Street suggests that buying in bleak times is a good idea. Sometimes this is true, but sometimes it is not. If you think now is a good time to buy oppressed AGNC investment (AGNC 1.57%) Since you expect the market to recover in the near future, here’s why you might want to reconsider.

Performance and price go in opposite directions

AGNC’s biggest attraction for most individual dividend investors will be its massive 20% dividend yield. It’s not a typo, but such high performance should be taken with a pinch of salt. In many cases, such increased returns indicate high risk. In this case, this risk poses a broad threat to the sustainability of the dividend.

Image source: Getty Images.

Basically, when the stock price falls, the dividend yield increases. After all, rate of return is a simple mathematical equation: annual dividend divided by stock price. With AGNC’s share price down more than 40% from its 52-week high, profitability has increased dramatically.

There’s a lot going on at AGNC today. As a mortgage real estate investment trust (REIT), it is struggling with difficulties resulting from, among other things, rising interest rates and a turbulent housing market. No wonder investors are in a gloomy mood. In fact, the entire REIT sector is currently in disfavor. However, there is a key metric for mortgage REITs that is very telling: book value per share.

For a mortgage REIT, book value is essentially the value of its portfolio of mortgage investments. Since it is essentially everything the company owns, book value is a very clear indication of what investors are buying. In the third quarter, AGNC had a book value of $8.08 per share. This is down from $9.39 at the end of the second quarter and $9.08 in the third quarter of 2022.

This is a very large decline in both cases and indicates that AGNC’s core business is under serious pressure, no matter how hard the company tries to emphasize the advantages. Even if there is a bull market and AGNC’s business starts to improve, it may not be enough to protect the dividend from a cut.

AGNC has a really bad dividend record

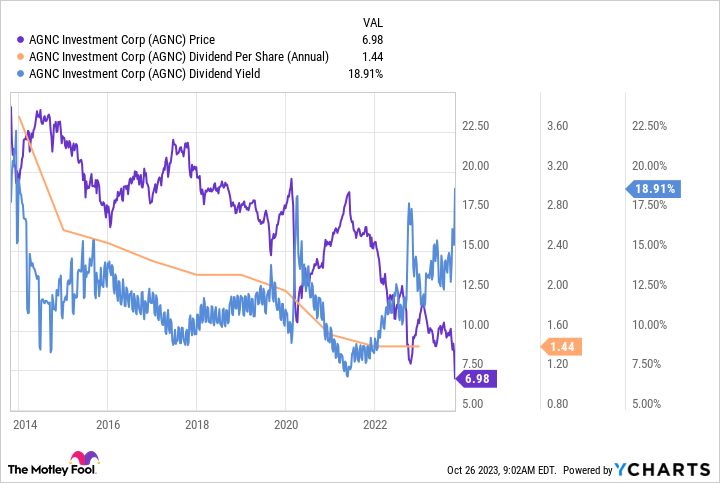

There are valid reasons to be concerned about the dividend, and it goes beyond the strain the company is currently under. A quick look back at the company’s dividend history shows just how high the potential risk is. As the orange line in the chart below shows, the dividend has been on a steady downward trend for a decade.

AGNC data by YCharts

However, note the purple line that is heading down with the dividend. This is the share price. Back to the dividend yield calculations, and you’ll see that AGNC’s dividend yield (blue line) is still in the double digits, even though the dividend continues to decline. This is not a good income story for investors who are trying to create a passive income stream to survive in retirement.

Sure, things can get better. The dividend may be maintained or even shifted towards growth. However, given history and the rapid decline in book value, the risk-reward ratio appears to be far too risk-biased for most investors.

There is a place for AGNC, but it probably isn’t in your portfolio

Mortgage REITs like AGNC are complex investments that most investors should probably avoid. History shows that it is simply not a reliable dividend stock. It is most suitable for institutional-level investors such as insurance companies who focus more on issues such as asset allocation because it provides direct exposure to mortgage lending.

Most individual investors seeking dividend income do not act like institutional investors. Even if a bull market is on the horizon, you’re probably better off staying away from AGNC Investment.

#bull #market #AGNC #Investment #dividend #stock #motley #fool

Image Source : www.fool.com