(Bloomberg) — U.S. corporate debt markets are showing early signs of weakness as rising yields and falling stock prices take their toll.

Most read by Bloomberg

Risk premiums, or spreads, on investment-grade corporate bonds rose to their highest level since June. In the junk bond market, where yields have risen to their highest level in a year, some companies are having a harder time selling debt. Venture Global LNG Inc., a liquefied natural gas supplier, was able to borrow $4 billion on Thursday only after paying more than initially expected.

Even in the asset-backed securities market, often viewed as a relatively low-risk market because bonds are asset-backed and have relatively short maturities, Mexican fast food chain Qdoba Restaurant Corp. had to cut its offer to $305 million from the originally planned $325 million.

And in the lending market, facilities management company BGIS withdrew a $916 million loan from a consortium in the first shelved deal since August. The loan was rated B and offered at 450 basis points over par, at a discount of 98 cents on the dollar.

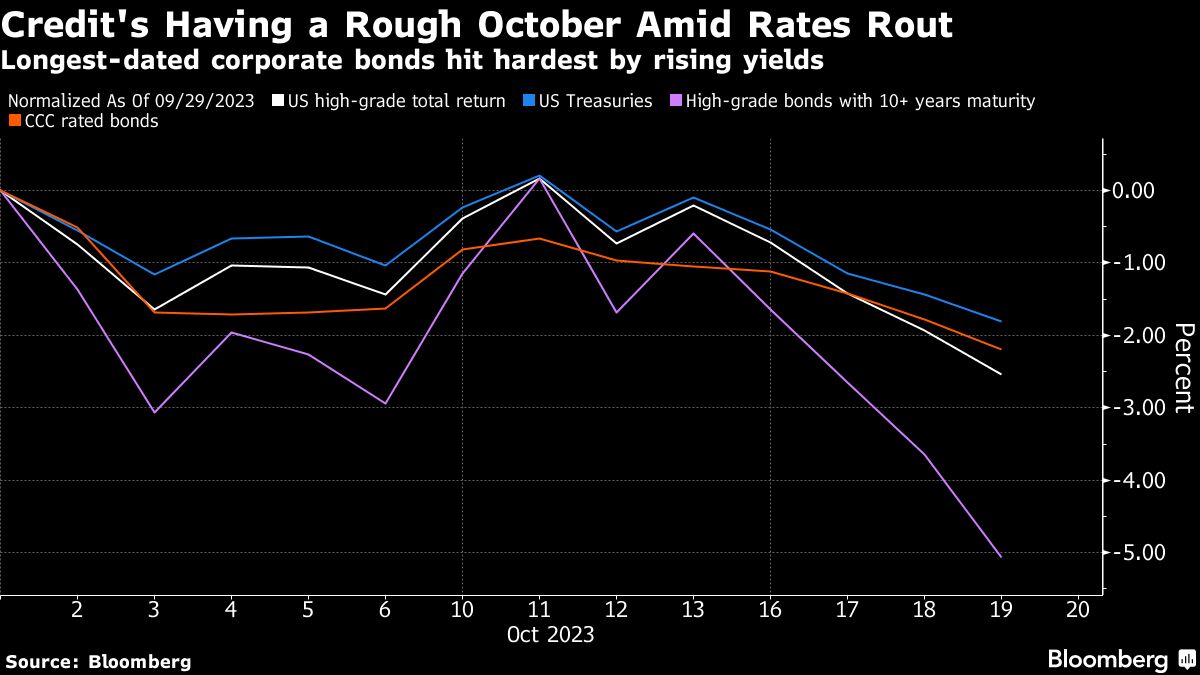

The sell-off in government bonds has spread to all corners of the corporate lending sector. Treasury yields rose this week to their highest levels in at least 16 years, with the 10-year Treasury rate nearing 5% on Thursday after stronger-than-expected retail sales data raised concerns that the Federal Reserve has more work to do performance when it comes to slowing down inflation. Treasury yields are falling on U.S. stock markets on Friday.

Still, investment-grade returns have hit their highest level since 2009, creating opportunities for investors who can stomach the volatility.

Read more: How Rising Interest Rates Restored America’s Debt Term Premiums: QuickTake

For a long-term investor, the level of entry into the fixed income market is very attractive, said Benoit Anne, chief strategist at MFS Investment Management. Investment-grade spreads don’t encourage buying, but the profitability picture is a once-in-a-lifetime opportunity.

However, this may not be good news for issuers, at least as interest rate volatility continues. Quotes of some of the bonds sold this week by companies such as Wells Fargo & Co., Goldman Sachs Group Inc. and JPMorgan Chase & Co. by Friday were wider than priced, indicating that issuers coming next week will have to offer larger concessions.

Other issuers in the leveraged loan market have also had to ease conditions to be able to borrow. A group of banks led by Morgan Stanley sold a $2.4 billion loan to Qlik Technologies Inc. on Thursday. backed by Thoma Bravo after changing the structure and improving the documents to make them more investor-friendly.

Even with this volatility, companies will still need to refinance in a market with higher interest rates. According to Goldman Sachs strategists, the amount of junk bonds maturing in the next 18-36 months is at the highest level since 2007.

For more than a decade, corporate bonds had very little competition from Treasury or mortgage-backed securities, but that dynamic changed dramatically and quickly, with all three markets offering competitive yields, Scott Kimball, managing director at Loop Capital Asset Management.

Read more: Blue chip profitability creates golden age of credit demand: Barclays

– With help from James Crombie, Olivia Raimonde, Caleb Mutui, Michael Gambale and Brian Smith.

(Update details regarding BGIS’s withdrawal of the term loan from the consortium in the fourth paragraph.)

Most read on Bloomberg Businessweek

2023 Bloomberg L.P

#rate #selloff #pervades #corners #credit #market

Image Source : finance.yahoo.com